Thus, the first challenge in building a DCF model is to define and calculate the cash flows that a business generates. There are two common approaches to calculating the cash flows that a business generates. We will discuss how to use the Gordon growth and H model in detail in later sections. Using the MadDonald case again, the $1000 cash outflow for buying the refrigerator is not counted as expense in the year in which it was paid because the $1000 was capitalized as a fixed asset on the balance sheet.

Key DCF Assumptions

- The problem with this approach is that you need quick access to data for comparable companies, which may be tricky without Capital IQ, FactSet, or similar services.

- The Discounted Cash Flow (DCF) model is a valuation method used to estimate the intrinsic value of a company.

- However, more often than not, we are more interested in the stock price than in this value.

- The terminal value is calculated in the terminal year and we will discuss more on how to do terminal value calculation later in this article.

- Discounted cash flow can help investors who are considering whether to acquire a company or buy securities.

After forecasting the expected cash flows, selecting a discount rate, discounting those cash flows, and totaling them, NPV then deducts the upfront cost of the investment from the DCF. For instance, if the cost of purchasing the investment in our above example were $200, then the NPV of that investment would be $248.68 minus $200, or $48.68. Two, select a discount rate, typically based on the cost of financing the investment or the opportunity cost presented by alternative investments. Three, discount the forecasted cash flows back to the present day, using a financial calculator, a spreadsheet, or a manual calculation. When a company analyzes whether it should invest in a certain project or purchase new equipment, it usually uses its weighted average cost of capital (WACC) as the discount rate to evaluate the DCF. The WACC incorporates the average rate of return that shareholders in the firm are expecting for the given year.

Dividend Discount Model (DDM)

Thus we need to deduct cash paid for these “investing activities” when calculating the cash flow for the year. Capital expenditure should also be projected when you prepare a forecast dcf model steps of the business (In our example it is provided ). The discounted cash flow model can also be used to value private companies that don’t have publically traded equity.

Understanding the DCF Calculator

As an equity analyst, rather than making our own assumptions, we can use a DCF model to ask the question “what has to be true for the current share price to be correct? ” This can give us a very useful insight into the cheapness/expensiveness of a share. As we all know, investor sentiment and market conditions can change dramatically, especially when the cost of capital shifts. If using the Gordon Growth Model, terminal value assumes constant rates of growth—which are obviously rare in reality.

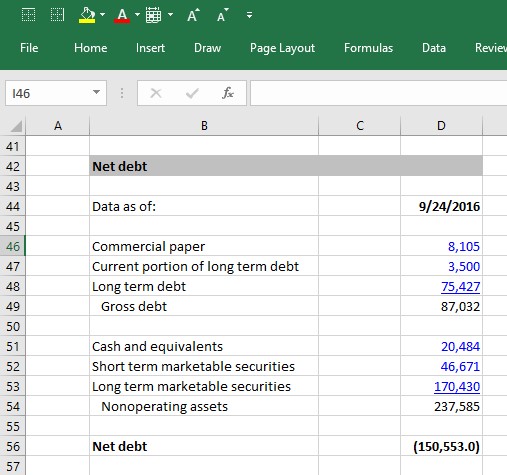

Calculating Equity Value: Adding the Value of Non-Operating Assets

Cash flow is required to finance the increase of working capital (and vice versa, cash will be released when working capital decreases). As cash flow is not captured in the income statement, we will need to adjust for these items in the DCF as well. Next you need to determine the Expected future cashflows from the Valuation Date onwards (since the DCF only incorporates future cash flows into the valuation). In other words, the DCF model discounts a company’s expected cash flows in order to arrive at a present value that reflects the time value of money. Once we have determined the value of each share, we can compare that value to the market’s current value (i.e. the current stock price). If the value we’ve calculated is higher than the current cost of the investment, then the investment is advisable.

In particular, the DCF model can be used to evaluate whether a proposed investment is likely to generate sufficient returns. The model can be used to value a company as a whole, or it can be used to value specific assets such as patents or real estate. This is due to the time value of money, which states that a dollar today is worth more than a dollar in the future because the dollar can be invested and will grow over time. That would indicate that the project cost would be more than the projected return. For DCF analysis to be useful, estimates used in the calculation must be as solid as possible.

In addition to the DCF model, there are other valuation methods that can be used to value a company. The terminal value is usually estimated using a multiple of earnings or cash flow. For example, if an investor requires a higher return, they can simply adjust the discount rate accordingly. This present value can then be compared to the current market price of the stock in order to determine whether it is under- or overvalued.

Unlike operating assets such as PP&E, inventory, and intangible assets, the carrying value of non-operating assets on the balance sheet is usually fairly close to their actual value. That’s because they are mostly comprised of cash and liquid investments that companies generally can mark up to fair value. That’s not always the case (equity investments are a notable exception), but it’s typically safe to simply use the latest balance sheet values of non-operating assets as the actual market values. A DCF model estimates a company’s intrinsic value (the value based on a company’s ability to generate cash flows) and is often presented in comparison to the company’s market value.